VAT Reverse Charging – What you need to know

Certain sales invoices will be subject to new VAT provisions. VAT Reverse Charging will apply to the following contracts.

• Those where the participants are subject to CIS.

• Those where the end-user (Employer) is retaining the built asset for their own use.

• Those where ‘sales’ comprise labour, material and/or plant.

• Those that may include an element of excluded sales but where those excluded items form part of the whole.

HMRC has produced an introductory webinar, The Association recommends members download the following flow-chart and then watch the first 30 mins of the webinar , the link follows:

1. Appendix one – HMRC’s Flowchart – To determine whether VAT reverse charging

applies and the elements of the process that need managing.

Contracting Members who are employed on a self-billing basis will have the reverse charging applied to their applications. The methodology as to how to mange outgoing and incoming invoices is illustrated below:-

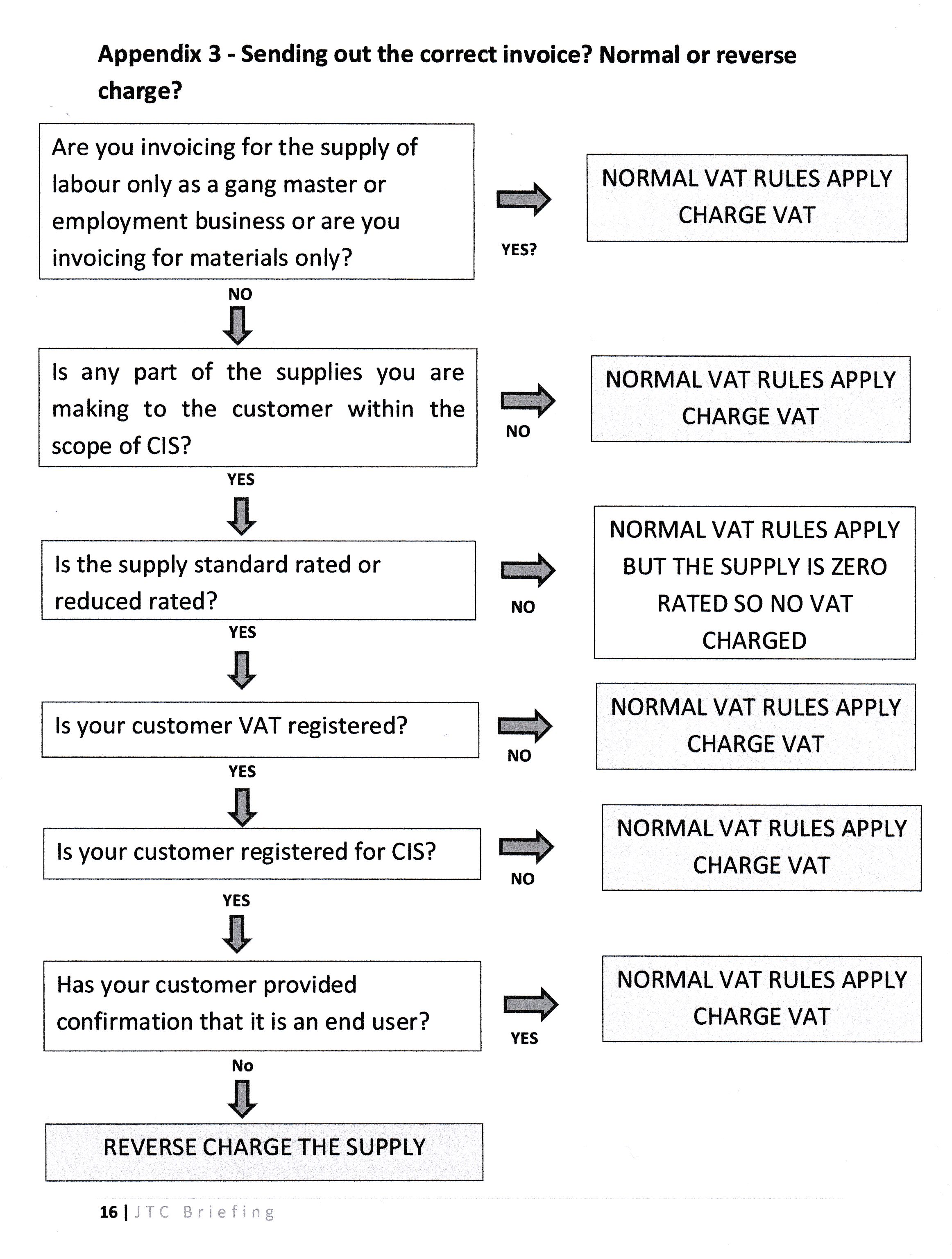

3. Appendix 3 – Flow Chart – Issuing a correct invoice.

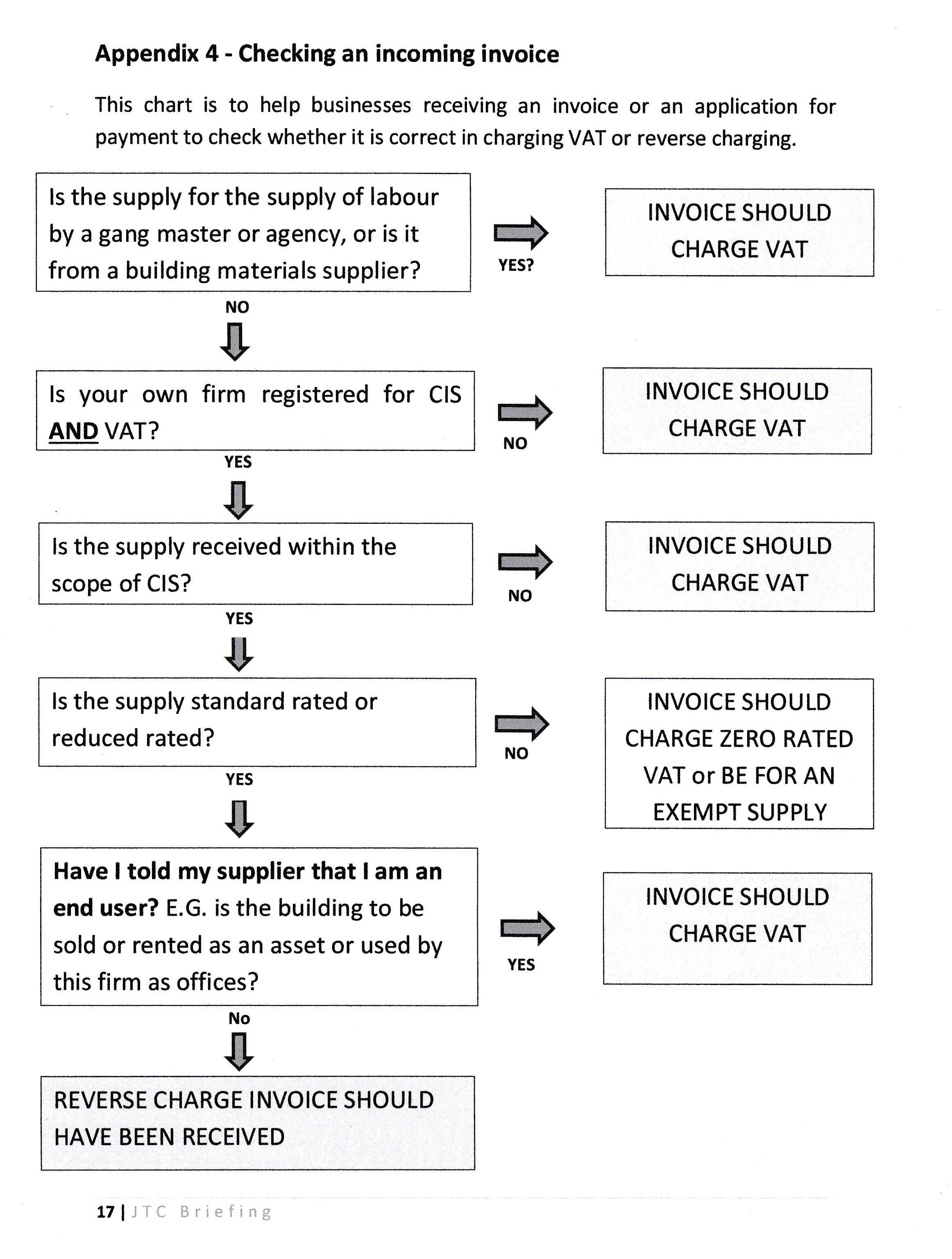

4. Appendix 4 – Flow Chart – Checking an Incoming Invoice.

VAT Reverse Charging will NOT apply to the following sales / contracts:

HMRC's approach to mixed supplies:

The legislation is designed so if there is a reverse charging ‘element’, in a supply, then the whole supply will be subject to Reverse Charging. A significant amount of communication will be required.

If in doubt, provided the recipient is VAT registered, and the payments are subject to CIS, it is recommended that the reverse charge should apply.

Members are advised to download our letter template to distribute it to their supply chain partners.

Further Assistance

Members who have a specific problem that cannot be answered utilising online resources, are encouraged to contact us at - candc@eca.co.uk . (The Enquiry should provide the Member’s full business title, Membership Number, primary point of contact and a range of times when contact can best be made.)

ECA has made special arrangements with a Tax Advisor to provide specialist advice and will administer any enquiry that members raise.

Read more

{kind=link}

{kind=link}