Compliance/ Corporate/ Tax

Our compliance, corporate and tax guidance will help Member businesses navigate the tricky landscape of regulatory requirements which arise in the electrotechnical and engineering services sector.

Invalid credentials, please check and try again.

Your account has not been verified by your nominated rep.

Your account has been suspended.

Sorry, an error occurred during registration. Please try again.

Your details have been passed to ECA and you will hear from us shortly.

Our compliance, corporate and tax guidance will help Member businesses navigate the tricky landscape of regulatory requirements which arise in the electrotechnical and engineering services sector.

It is vital that Members stay up to date with changes in regulations which could affect their businesses, particularly as they grow, to ensure they meet the requirements to go for bigger projects as well as protect themselves from potential penalties and reputational damage caused by non-compliance.

| Artifical Intelligence: Template | Nov 2025 |

| Artifical Intelligence: Overview | Nov 2025 |

| Corporate: Updated Requirements for Companies House Filings | Oct 2025 |

| Corporate: Modern Slavery Law Obligations | Aug 2025 |

| Building Safety Act: Overview | Jun 2025 |

| Building Safety Act: The Higher-Risk Building Regime | Jun 2025 |

| Building Safety Act: Principal Dutyholders | Jun 2025 |

| Building Safety Act: The Dutyholder Regime | Jun 2025 |

| Insurance: Trade Credit Insurance | May 2024 |

| Insurance: Construction and FM Insurance | Apr 2022 |

| Insurance: Professional Indemnity Insurance | Mar 2022 |

| Compliance: Data Protection Registration Fee | Mar 2020 |

| Compliance: Competition Law | Feb 2020 |

| Tax: Anti-Tax Evasion | Aug 2025 |

| Tax: Construction Industry Scheme | Jul 2024 |

| Tax: Reverse Charge VAT (FAQs) | Dec 2020 |

| Tax: Making Tax Digital | Mar 2020 |

| Tax: Reverse Charge VAT (JTC Guidance) | Jun 2019 |

| Tax: Reverse Charge VAT (Terminology) | Jul 2019 |

| Tax: Anti-Tax Evasion Policy | Aug 2025 |

| Tax: Reverse Charge VAT: Flow Chart | Jan 2021 |

| Tax: Reverse Charge VAT: Cash Flow Model | Oct 2019 |

| Tax: Reverse Charge VAT: Simple Cash Flow Calculator | Oct 2019 |

ECA has teamed up with Markel Tax to bring you FREE additional support in the area of tax advice

Call 03333 211 781 for advice from Markel Busienss Hub on tax issues (use your ECA membership name and number when calling).

Markel’s professional team offers phone advice/support on, amongst other areas:

You may find sector specific guidance and templates within ECA’s website here. If not you also have access to Markel’s Business Hub log in below for the code.

Please note: Markel are an independent third party partner to ECA. When accessing their services via ECA, you may have to set up an account directly with Markel citing your ECA membership credentials.

ECA Members’ access to the Markel Business Hub will grant access to the following areas:

Making Tax Digital (MTD) is the biggest change to tax reporting since self assessment launched 30 years ago.

From 6 April 2026, Members must use MTD for Income Tax if all of the following apply:

“Qualifying income” is the total income you get in a tax year from self-employment and property. HMRC guidance on how to work out your qualifying income can be found here.

Once you have signed up for MTD for Income Tax, you will need to use this system to create, store and correct digital records of your self-employment and property income and expenses, send your quarterly updates to HMRC, submit your tax return and pay tax due by 31 January the following year.

Exemptions

There are two types of exemption from MTD for Income Tax;

The key permanent exemptions are for those whose qualifying income is £20,000 or less or those who are digitally excluded, meaning it would not be reasonable for you to use MTD compatible software. You can find out if you qualify for being digitally excluded here.

You are automatically exempt until April 2027 if your 2024 to 2025 tax return showed that you either:

You will need to apply for a temporary exemption if your 2024 to 2025 tax return did not show this but your 2026 to 2027 tax return does so.

There are some other specific circumstances which could lead to a permanent or temporary exemption which are listed on HMRC’s website, here.

HMRC Guidance

HMRC has a number of other helpful guidance pages on MTD which Members are encouraged to become familiar with. These are linked below:

Sales may attract a sales tax, in the UK we call this tax VAT.

Works, in a variety of locations and for a variety of customers can attract a number of different sales tax rates, including exempt, zero rated, partial or lower rated, to or a standard rating. HMRC expects every business to know which rate is applicable to them and if necessary, to prove the rate charged to their customers is correct.

It is important that if there is any doubt as to the correct rate then HMRC’s guidance must be sought and reliance on any direction must only be made on written evidence

VAT is a very complex area of law and specialist advice may be required where works are being considered which do not clearly fall into a specific category.

The following is given by way of example: The shell of a building (structure and cladding) used in new construction is considered, for VAT purposes, as ‘alteration works’ if at least two walls are retained. ‘Granny annexes’ when sold as part of a dwelling are not to be treated as a separate commodity. A new build annexe to a charitable building would be treated as zero-rated if it has an independent means of access and it could function independently of the original building. Knowledge of these stipulations may may be valuable when tendering a design and build project.

HMRC’s website has guidance under ‘Buildings and Construction’ or try the www.nibusinessinfo.co.uk which also has useful information.

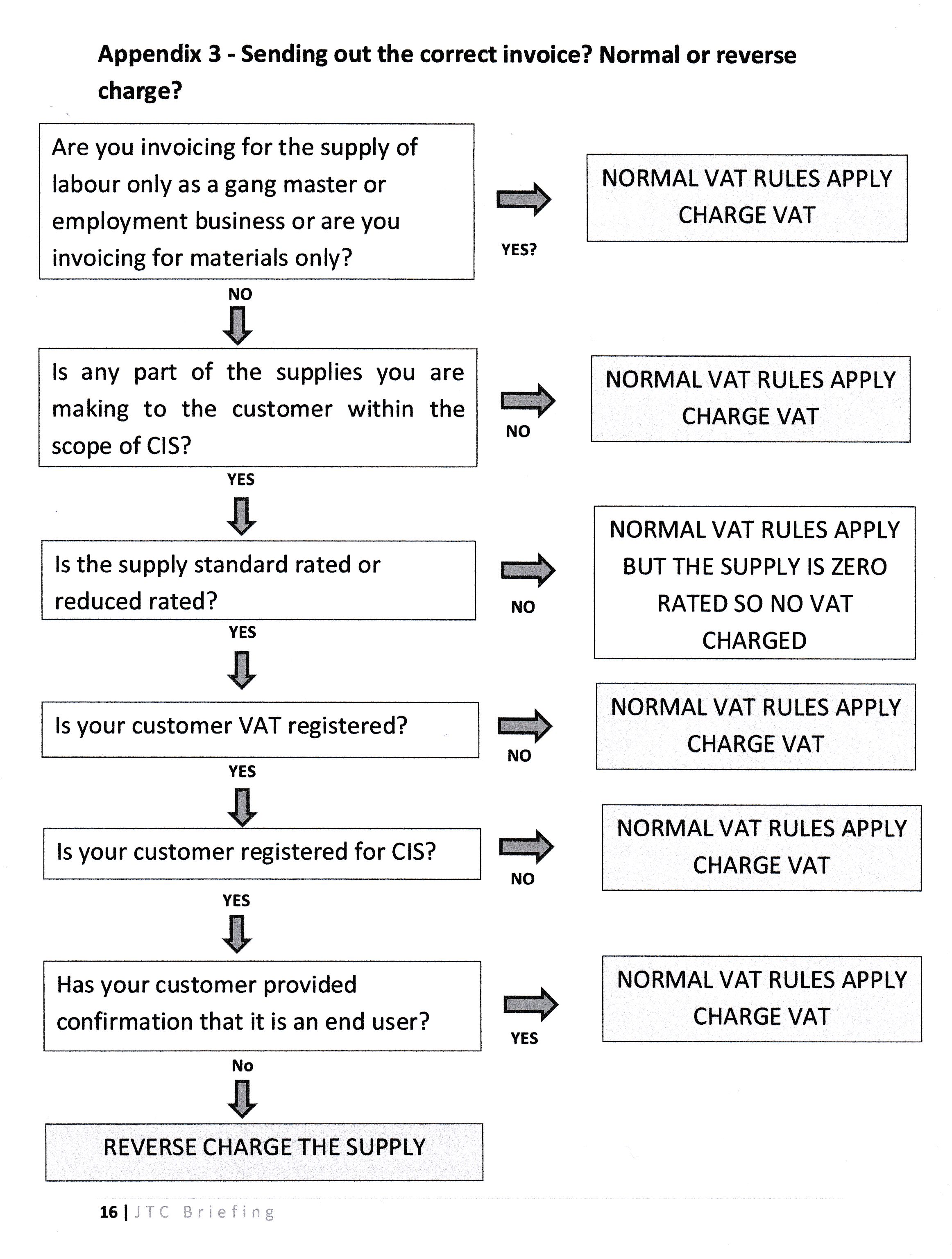

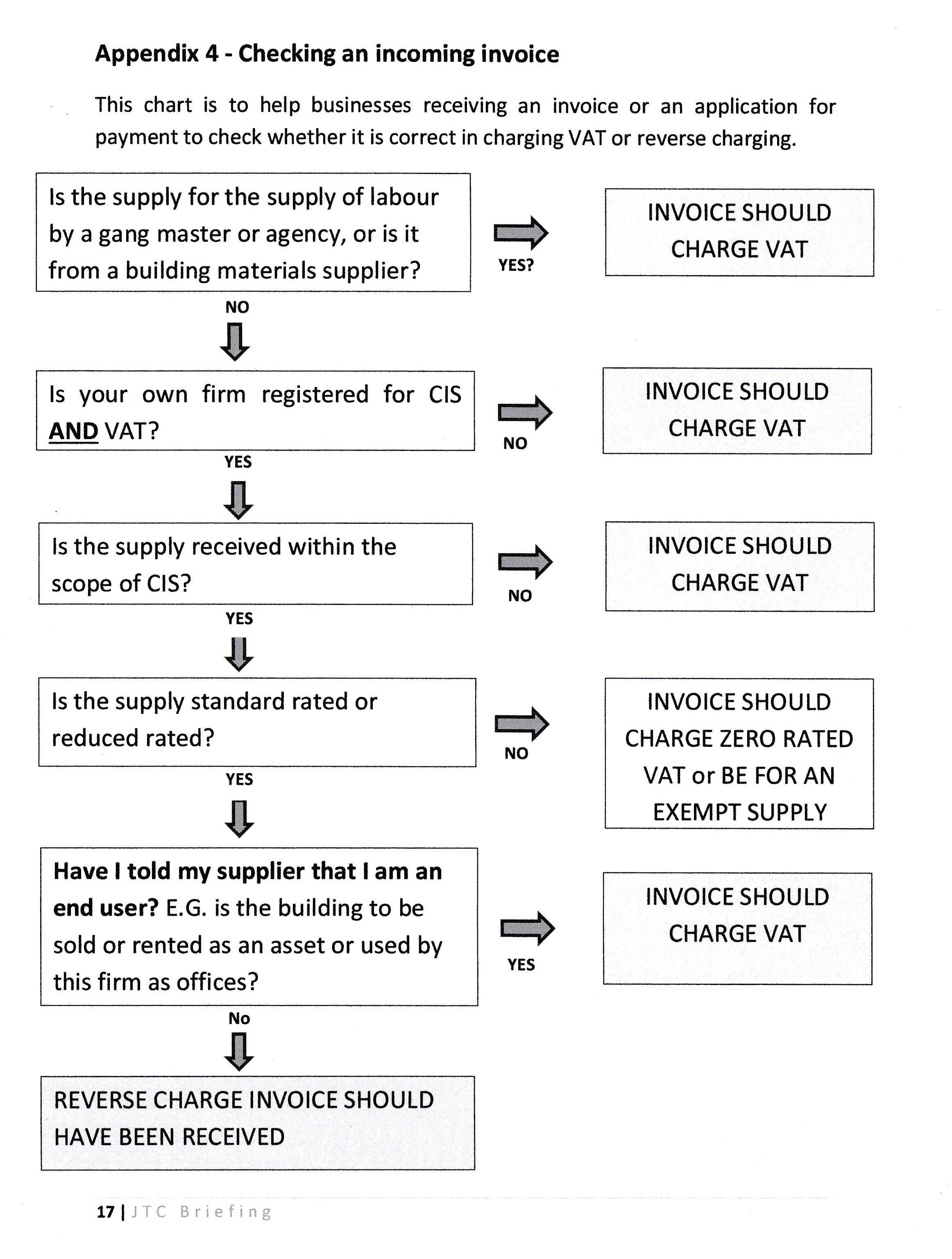

Certain sales invoices will be subject to new VAT provisions. VAT Reverse Charging will apply to the following contracts.

HMRC has produced an introductory webinar, which ECA recommends Members watch the first 30 minutes of, as well as downloading the following flow-chart:

Contracting Members who are employed on a self-billing basis will have the reverse charging applied to their applications. The methodology as to how to mange outgoing and incoming invoices is illustrated below:-

Sales entirely consistent of supply-only assets.

Sales entirely comprising of the installation of security systems (burglar alarm) closed circuit television and public address systems.

The legislation is designed so if there is a reverse charging ‘element’, in a supply, then the whole supply will be subject to Reverse Charging. A significant amount of communication will be required.

If in doubt, provided the recipient is VAT registered, and the payments are subject to CIS, it is recommended that the reverse charge should apply.

The Construction Industry Scheme (CIS) sets out the rules for how payments to subcontractors for construction work must be handled by contractors in the construction industry and excellent information is available from the HMRC website.

The tax authorities provide the industry with a number of online support services For a full introduction to how CIS may affect you, please visit the HMRC website.

HMRC provide a guide to CIS for Contractors and Subcontractors (Re: CIS 340).

While considering Tax Status, it is important to check the employment status of your subcontractors. You can do this by completing the online status indicator (ESI) found on the HMRC website.

Contractors employed in Construction work must register with CIS. The CIS Scheme covers most construction work and contractors who pay subcontractors must be registered.

As of 6 April 2021 the CIS Scheme changed, as follows:

In brief this means, that from the 6 April 2021:

HMRC’s explanation and summary of these changes can be found on the HMRC’s website search: Changes to tackle Construction Industry Scheme abuse.

All businesses require insurance to comply with their statutory requirements, meet their contractual obligations and help manage the risks to which they are exposed. And with Building Services Contractors undertaking an increasingly diverse and complex range of activity, having the right cover for your business is vital.

Founded in 1976 to insure ECA Members, Markel provides specialist liability and property insurance for electrical and mechanical building services engineers and contractors. Over 90% of the business written by ECIC is from independent insurance intermediaries appointed to find the best combination of service, price and cover for their clients.

For more information about Markel’s specialist products and services, ask your insurance broker to contact Markel or visit uk.markel.com.

{kind=link}

{kind=link}